TruckElectric

Well-known member

- First Name

- Bryan

- Joined

- Jun 16, 2020

- Threads

- 772

- Messages

- 2,488

- Reaction score

- 3,280

- Location

- Texas

- Vehicles

- Dodge Ram diesel

- Occupation

- Retired

- Thread starter

- #1

Matt Bohlsen

Trend Investing

Trend Investing finds the "next big thing" and the best ways to invest.

(18,697 followers)

Summary

Tesla's battery targets for Tesla and their targets for the global battery industry to support a 100% EV and 100% renewable energy world in 2030.

20TWh pa of global battery demand in 2030 (10TWh EVs, 10TWh storage) will need 55x more lithium (than 2019 levels), 20x more cobalt, 26x more graphite, and 7x more nickel.

All this should mean that the 2020's decade should be a super-cycle decade for battery metal miners, especially post 2023 as demand surges with EV/ICE parity.

I do much more than just articles at Trend Investing: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

This article first appeared in Trend Investing on Oct. 7, 2020, but has been updated for this article.

At Tesla (TSLA) Battery Day, the company announced they plan to grow their battery production to 3TWh by 2030. Tesla say the globe will need 10TWh pa battery capacity for electric vehicles (EVs) and 10TWh pa for energy storage by 2030.

Tesla's battery demand represents a 86 fold increase. Yes you read that right. A 86 fold increase in Tesla's battery production capacity this decade (from 2019 to 2030), allowing Tesla to produce 20 million EVs pa and energy storage products by 2030.

That also means Tesla will need to source directly and indirectly (other battery suppliers to Tesla) more battery materials on a scale never seen before in history.

Tesla Battery Day forecasts (about 'Tesla's' targets)

Source: Tesla Battery Day video

Source: Tesla Battery Day video

Note: Musk said that in total he thinks 20-25TWh pa of batteries (he is including the 10TWh pa for EVs and at least 10TWh pa for the grid) is needed for about 15-20 years to electrify the fleet and make the grid function on 100% renewable energy supported by energy storage

Bloomberg's forecast prior to Tesla Battery Day

Annual Li-ion global battery demand forecast to grow about 10x this decade to 2TWh. Since Tesla Battery Day this will most likely be revised substantiallyhigher as Tesla alone plan to reach 3TWh (3,000GWh) by 2030, and say the world will need a total of 20TWh (10+10) pa by 2030. That's a 10x increase on Bloomberg's forecast. This could potentially large upgrade when the next Bloomberg forecast comes out.

Source

Based on the Bloomberg chart above, a shift from 230GWh in 2019 to 20TWh by 2030 is a 86x increase.

Or calculated another way to go from 2.2m EVs pa to 90m EVs pa is a 41 fold increase, then add in energy storage, and again we get somewhere near a 86x increase in global battery demand this decade. This all assumes that by 2030 we have moved to 100% new cars sold are EVs, and all new energy is renewable with battery storage by 2030.

The impact on global EV metals demand by 2030 if Tesla's forecast of 100% EVs (10TWh pa batteries) and 100% renewable energy with storage (10TWh pa batteries) is correct

First I look at just Tesla's demand (first chart below), then total global demand (second chart below).

EV metals needed pa by Tesla by 2030 to reach 3TWh pa of batteries compared to Tesla 2019 demand

Looking at the excel chart above it shows that if Tesla goes from 0.035TWh (35GWh) of battery production in 2019 to their target of 3TW battery production by 2030 (86-87x increase) it has the following implications for Tesla's demand:

EV metals needed pa by the world by 2030 to reach 20TWh pa of batteries compared to total "global" demand at end 2019

Source: My own excel calculations. I may soon add in manganese demand.

Looking at the excel chart above it shows that if global battery demand goes from 0.230TWh (230GWh) of battery production in 2019 to the Elon Musk target of 20TW battery production by 2030 (87x increase) it has the following implications for global demand:

The impact on demand for the various EV metals in a 100% EV world

Source: Visual Capitalist courtesy of UBS

The UBS in a 100% EV world (does not factor in energy storage) forecasts were:

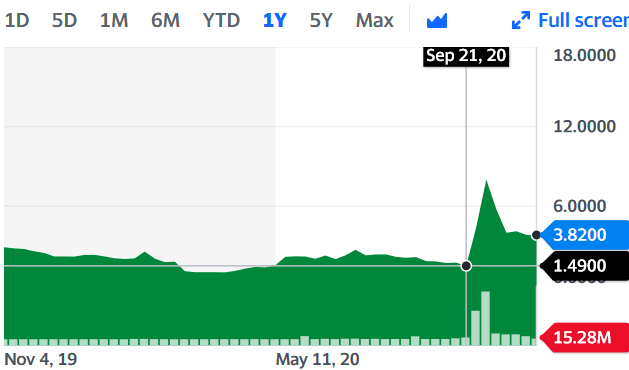

North American EV miners moved higher - Westwater Resources is up 2.6x since Tesla battery day on Sept. 22, 2020

Source

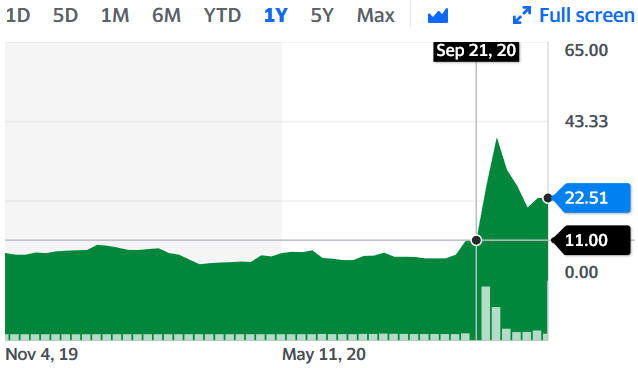

Piedmont Lithium up 2x since Tesla Battery Day

Source

Risks/Notes

BMI Simon Moores states:

There are a number of takeaways from the Tesla Battery Day targets. The targets are much higher (10x higher than Bloomberg) than ever before and are extremely bullish. This is because Musk says Tesla plans to "accelerate" the transition to sustainable energy and EVs at a much faster pace than was previously thought possible. Their 3TWh target (say 2TWh for EVs) for 2030 would be 20% of their global EV target of 10TWh, implying a possible 20% market share for Tesla EVs in 2030. It may end up being higher if other OEMs continue to drag their feet.

In the risks section I discuss that it's unlikely we will reach 100% EV market share by 2030, or be at a 100% renewable energy/grid storage by 2030.

For Tesla they now see they will need to massively scale up to terafactories, ideally matching the same continent where they sell their EVs and ES products. Running the numbers in excel shows how profound the impact could be. In fact the EV metals demand surge would be absolutely enormous and almost certainly limited by EV metals supply. Can anyone supply Tesla with 86x more lithium (than 2019 levels), 43x more cobalt, 86x more graphite, and 58x more nickel? Little wonder Musk is talking to every large nickel miner right now, and has signed lithium deals with multiple companies. The same will likely apply for cobalt and graphite.

For global demand, based on Tesla's target of 20TWh pa of battery demand in 2030 (10TWh EVs, 10TWh grid storage), the globe will need 55x more lithium (than 2019 levels), 20x more cobalt, 26x more graphite, and 7x more nickel. Lithium is the highest as it's in both EVs and ES and the lithium market is small. Nickel is the lowest due to perhaps no nickel in future energy storage products (LFP instead) and the nickel market already is very big.

These numbers are larger than the UBS 100% EV world scenario as they also factor in energy storage demand to get to a 100% renewable energy grid.

While it's highly likely that these grand targets will not be met, even if the global targets were only 50% met, there would be a massive tsunami of demand for EV metals accelerating each year this decade. I would think that lithium, cobalt, graphite, and nickel supply would not be able to even come close to keeping up to this scale of demand ramp.

All this should mean that the 2020's decade should be a super-cycle decade for battery metal miners, especially post 2023 as demand surges with EV/ICE parity. For now some North American EV metal miners stock prices have surged higher (Westwater Resources (WWR) - 2.6x higher, Piedmont Lithium (PLL) - 2x higher). The good news is that we are just at the beginning and the massive demand surge ahead should lift most battery metal miners much higher.

SOURCE: Seeking Alpha

Trend Investing

Trend Investing finds the "next big thing" and the best ways to invest.

(18,697 followers)

Summary

Tesla's battery targets for Tesla and their targets for the global battery industry to support a 100% EV and 100% renewable energy world in 2030.

20TWh pa of global battery demand in 2030 (10TWh EVs, 10TWh storage) will need 55x more lithium (than 2019 levels), 20x more cobalt, 26x more graphite, and 7x more nickel.

All this should mean that the 2020's decade should be a super-cycle decade for battery metal miners, especially post 2023 as demand surges with EV/ICE parity.

I do much more than just articles at Trend Investing: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

This article first appeared in Trend Investing on Oct. 7, 2020, but has been updated for this article.

At Tesla (TSLA) Battery Day, the company announced they plan to grow their battery production to 3TWh by 2030. Tesla say the globe will need 10TWh pa battery capacity for electric vehicles (EVs) and 10TWh pa for energy storage by 2030.

Tesla's battery demand represents a 86 fold increase. Yes you read that right. A 86 fold increase in Tesla's battery production capacity this decade (from 2019 to 2030), allowing Tesla to produce 20 million EVs pa and energy storage products by 2030.

That also means Tesla will need to source directly and indirectly (other battery suppliers to Tesla) more battery materials on a scale never seen before in history.

Tesla Battery Day forecasts (about 'Tesla's' targets)

- Musk plans for Tesla to grow Li-ion battery production capacity from about 35GWh pa in 2019 to 3TWh (3,000Gwh) in 2030. That's an incredible 86x increase in a decade.

- Tesla to increase EV production from ~500K pa in 2020 to about 20m by 2030 for a 40x increase in a decade.

- Tesla to massively ramp up energy storage products and solar this decade.

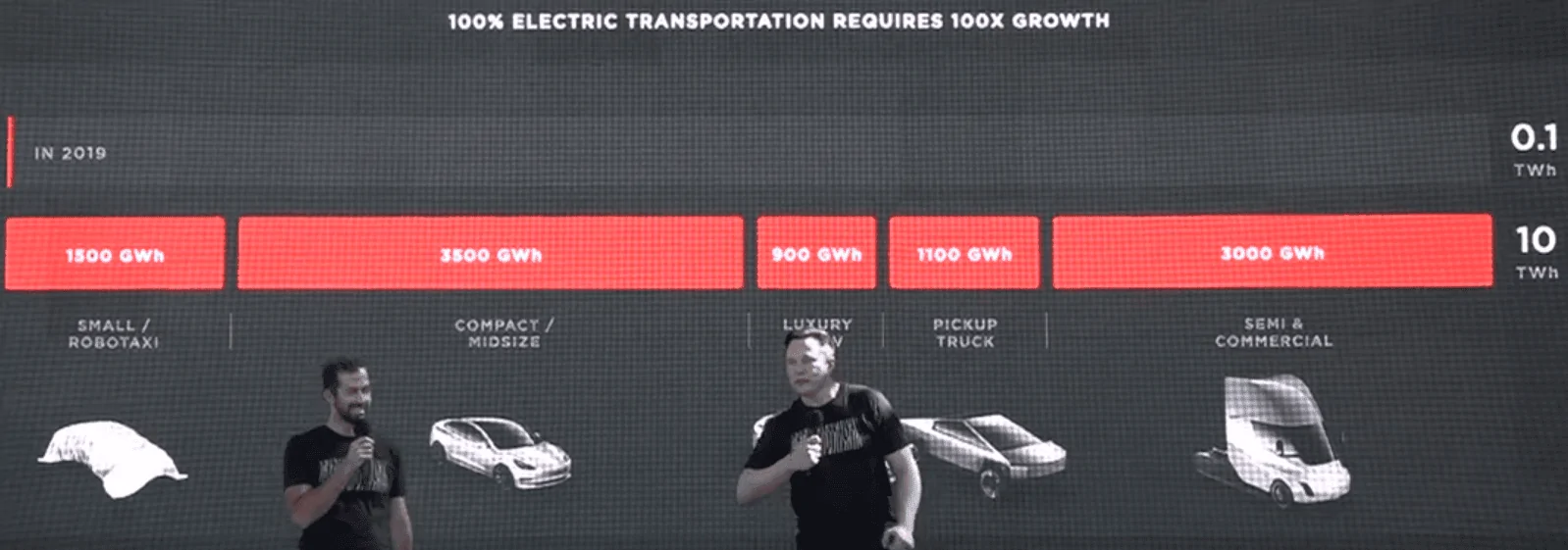

- For electric vehicles - Global battery production for electric transportation needs to grow 100x to reach 10TWh pa then do that for 15 years to reach 150TWh cumulative production to achieve a 100% electric global fleet of vehicles.

Source: Tesla Battery Day video

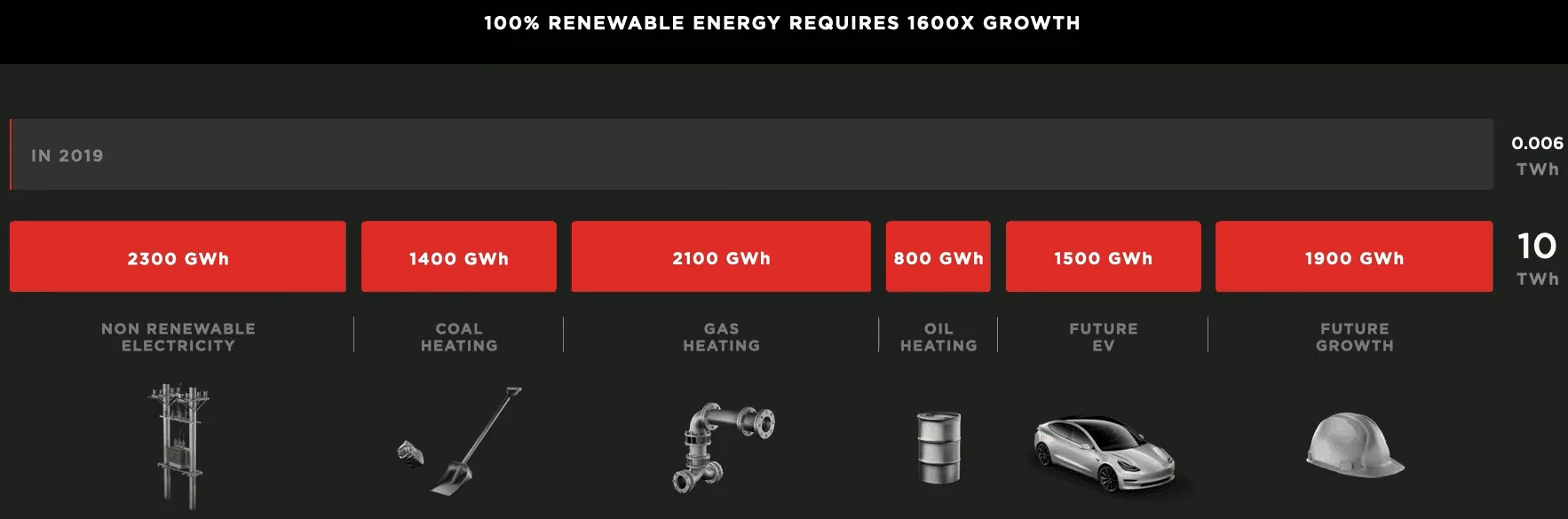

- For a 100% global renewable energy electricity grid - At least 10TWh pa of batteries to support the grid is needed to be 100% renewable, and done for about 20 years. That's a 1,600x increase on 2019 levels.

Source: Tesla Battery Day video

Note: Musk said that in total he thinks 20-25TWh pa of batteries (he is including the 10TWh pa for EVs and at least 10TWh pa for the grid) is needed for about 15-20 years to electrify the fleet and make the grid function on 100% renewable energy supported by energy storage

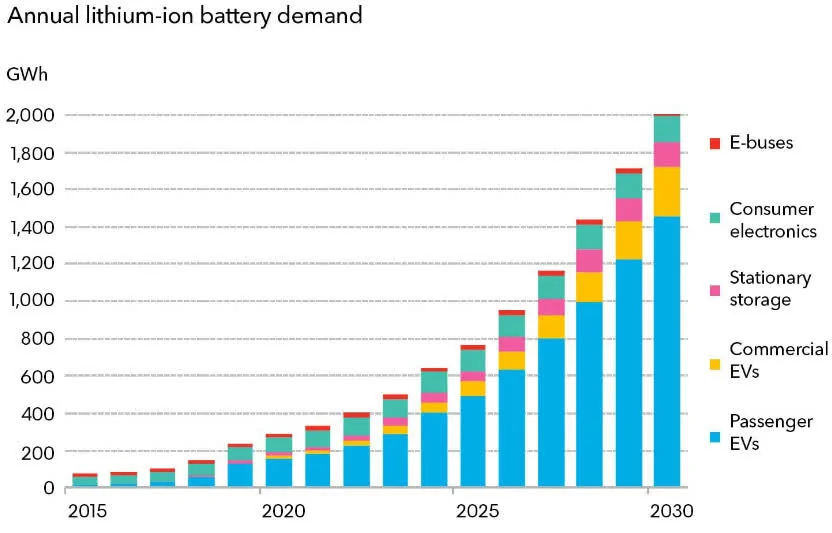

Bloomberg's forecast prior to Tesla Battery Day

Annual Li-ion global battery demand forecast to grow about 10x this decade to 2TWh. Since Tesla Battery Day this will most likely be revised substantiallyhigher as Tesla alone plan to reach 3TWh (3,000GWh) by 2030, and say the world will need a total of 20TWh (10+10) pa by 2030. That's a 10x increase on Bloomberg's forecast. This could potentially large upgrade when the next Bloomberg forecast comes out.

Source

Based on the Bloomberg chart above, a shift from 230GWh in 2019 to 20TWh by 2030 is a 86x increase.

Or calculated another way to go from 2.2m EVs pa to 90m EVs pa is a 41 fold increase, then add in energy storage, and again we get somewhere near a 86x increase in global battery demand this decade. This all assumes that by 2030 we have moved to 100% new cars sold are EVs, and all new energy is renewable with battery storage by 2030.

The impact on global EV metals demand by 2030 if Tesla's forecast of 100% EVs (10TWh pa batteries) and 100% renewable energy with storage (10TWh pa batteries) is correct

First I look at just Tesla's demand (first chart below), then total global demand (second chart below).

EV metals needed pa by Tesla by 2030 to reach 3TWh pa of batteries compared to Tesla 2019 demand

Looking at the excel chart above it shows that if Tesla goes from 0.035TWh (35GWh) of battery production in 2019 to their target of 3TW battery production by 2030 (86-87x increase) it has the following implications for Tesla's demand:

- A 86x increase in lithium demand.

- A 43x increase in cobalt demand.

- A 86x increase in graphite demand.

- A 58x increase in nickel demand.

EV metals needed pa by the world by 2030 to reach 20TWh pa of batteries compared to total "global" demand at end 2019

Source: My own excel calculations. I may soon add in manganese demand.

Looking at the excel chart above it shows that if global battery demand goes from 0.230TWh (230GWh) of battery production in 2019 to the Elon Musk target of 20TW battery production by 2030 (87x increase) it has the following implications for global demand:

- A 55x increase in lithium demand.

- A 20x increase in cobalt demand.

- A 26x increase in graphite demand.

- A 7x increase in nickel demand.

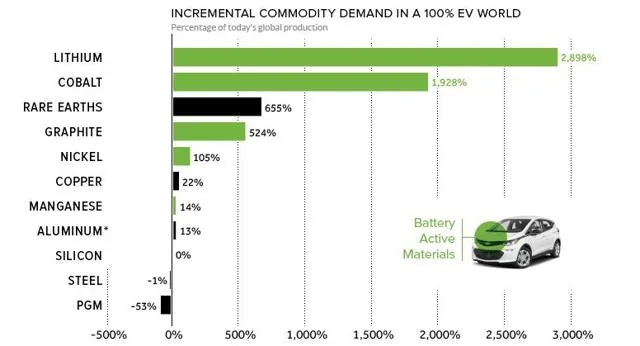

The impact on demand for the various EV metals in a 100% EV world

Source: Visual Capitalist courtesy of UBS

The UBS in a 100% EV world (does not factor in energy storage) forecasts were:

- A 29x increase in lithium demand.

- A 19x increase in cobalt demand.

- A 5x increase in graphite demand.

- A 105% increase in nickel demand.

North American EV miners moved higher - Westwater Resources is up 2.6x since Tesla battery day on Sept. 22, 2020

Source

Piedmont Lithium up 2x since Tesla Battery Day

Source

Risks/Notes

- Musk's targets are extremely bullish. For example 10TWh pa of batteries can supply 100m EVs with 100kWh batteries. What if the average EV battery capacity was only 50kWh, that would mean we only need 5TWh pa by 2030 for EVs. We may still need 10TWh pa for energy storage.

- It's unlikely we will reach 100% EV market share by 2030, or be at a 100% renewable energy/energy storage grid by 2030.

- Benchmark Mineral Intelligence says we are now at 167 gigafactories (85are now operational) in the pipeline to 2029 and all are competing for the same raw material. The 167 gigafactories represent about 3TWh of capacity by 2029, still well short of the 20TWh capacity Musk says we will need by 2030.

BMI Simon Moores states:

ConclusionBoth quantity and quality of lithium, cobalt and nickel will be Tesla’s biggest hurdles to get right. Graphite anode and manganese will also come with their own sourcing challenges.

There are a number of takeaways from the Tesla Battery Day targets. The targets are much higher (10x higher than Bloomberg) than ever before and are extremely bullish. This is because Musk says Tesla plans to "accelerate" the transition to sustainable energy and EVs at a much faster pace than was previously thought possible. Their 3TWh target (say 2TWh for EVs) for 2030 would be 20% of their global EV target of 10TWh, implying a possible 20% market share for Tesla EVs in 2030. It may end up being higher if other OEMs continue to drag their feet.

In the risks section I discuss that it's unlikely we will reach 100% EV market share by 2030, or be at a 100% renewable energy/grid storage by 2030.

For Tesla they now see they will need to massively scale up to terafactories, ideally matching the same continent where they sell their EVs and ES products. Running the numbers in excel shows how profound the impact could be. In fact the EV metals demand surge would be absolutely enormous and almost certainly limited by EV metals supply. Can anyone supply Tesla with 86x more lithium (than 2019 levels), 43x more cobalt, 86x more graphite, and 58x more nickel? Little wonder Musk is talking to every large nickel miner right now, and has signed lithium deals with multiple companies. The same will likely apply for cobalt and graphite.

For global demand, based on Tesla's target of 20TWh pa of battery demand in 2030 (10TWh EVs, 10TWh grid storage), the globe will need 55x more lithium (than 2019 levels), 20x more cobalt, 26x more graphite, and 7x more nickel. Lithium is the highest as it's in both EVs and ES and the lithium market is small. Nickel is the lowest due to perhaps no nickel in future energy storage products (LFP instead) and the nickel market already is very big.

These numbers are larger than the UBS 100% EV world scenario as they also factor in energy storage demand to get to a 100% renewable energy grid.

While it's highly likely that these grand targets will not be met, even if the global targets were only 50% met, there would be a massive tsunami of demand for EV metals accelerating each year this decade. I would think that lithium, cobalt, graphite, and nickel supply would not be able to even come close to keeping up to this scale of demand ramp.

All this should mean that the 2020's decade should be a super-cycle decade for battery metal miners, especially post 2023 as demand surges with EV/ICE parity. For now some North American EV metal miners stock prices have surged higher (Westwater Resources (WWR) - 2.6x higher, Piedmont Lithium (PLL) - 2x higher). The good news is that we are just at the beginning and the massive demand surge ahead should lift most battery metal miners much higher.

SOURCE: Seeking Alpha

Sponsored